Close

Leave Feedback

Welcome to the new btim.com.auTake a two minute tour to see what we've changed

Hi there! Welcome to the new look Pendal website... Take a two minute tour to see what we’ve changed.

Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

The Point

Quick, actionable insights for investors

May 29

The headlines driving Aussie equities | Falling USD should lift EMs | Where to find opportunities in theme-driven markets

Loading posts...

Elise McKay: The headlines driving Aussie equities this week

Quick view

Elise McKay: The headlines driving Aussie equities this week

Here are the main factors driving the ASX this week, according to Aussie equities analyst and portfolio manager ELISE MCKAY and reported by head investment specialist CHRIS ADAMS

Read Pendal’s latest weekly equities overview.

Crispin Murray: Where to find ASX opportunities amid ‘theme-driven’ market noise

Quick view

Crispin Murray: Where to find ASX opportunities amid ‘theme-driven’ market noise

Share prices are increasingly moved by popular themes like AI disruption, trade wars, and tariff fears – without regard to company fundamentals or long-term valuations.

As a result, quality Australian companies with sound outlooks and predictable cash flows are being indiscriminately sold off.

That’s creating opportunities for active fund managers, Pendal’s head of equities Crispin Murray told Morningstar’s 2025 investment conference in Sydney last week.

“We believe this is creating more distortions in the market. It means the amplitude of mispricing is greater, and it lasts longer.”

Global market dislocation means the ASX has a range of industrial companies with predictable cash flows and returns that have been sold down and offer opportunities for investors, he says.

“One example is CSL – one of Australia’s largest, most successful companies. Five years ago it was running high – at an over-40 multiple. It’s now down to about 22 times earnings,” he says.

Fears of the impact of tariffs on CSL are misplaced, assuming the company doesn’t do anything to respond – “and I think that’s where the market’s overreacting,” argues Crispin.

“We think the risk on the tariff front is being overstated, and that’s what’s providing you the opportunity.” Pendal owns CSL.

Read more

‘Emerging markets crisis’? That’s a wildly overstated view, say our experts

Quick view

‘Emerging markets crisis’? That’s a wildly overstated view, say our experts

Some analysts have described a pattern of a weaker dollar and rising bond yields in the US as a ‘classic emerging markets crisis’.

“As veterans of actual emerging crises dating back to 1994, we consider that view to be wildly overstated,” writes Pendal’s EM team in their latest analysis.

In spite of volatility and weakness in core US financial markets, the currencies of almost all emerging markets strengthened against the US dollar in March and April. Meanwhile bond yields fell for the majority of major EMs.

“Emerging markets are driven by two major global drivers: international capital flows and international trade.

“A weaker dollar represents capital flowing out of the US and into the rest of the world – and a weaker dollar has consistently been positive for emerging markets over the past 30 years.

“Although evolving tariff policies threaten a downturn in global trade, the message from financial markets is that investor uncertainty about US economic policies is a clear positive for emerging economies and for investors in emerging markets.”

Read more

Amy Xie Patrick: China, the US, and the value of uncertainty

Quick view

Amy Xie Patrick: China, the US, and the value of uncertainty

This month’s divergence in US and China rates policies wasn’t just a curiosity for money managers, observes Pendal’s head of income strategies, Amy Xie Patrick.

“It’s a study in contrasts, a reflection of deeper structural differences, and a reminder that policy effectiveness doesn’t always come wrapped in transparency or even democracy,” says Amy in her latest markets analysis.

On May 7, the US Fed left rates unchanged despite growing political pressure. Meanwhile, the People’s Bank of China delivered another dose of stimulus.

“One central bank faced market criticism over its non-committal guidance,” notes Amy. “The other moved swiftly and silently, without needing to justify its decision.

“Perhaps the most contrarian yet valuable takeaway is that less policy guidance may be a good thing.

“By avoiding the hard task of forecasting far into the future, we free ourselves from unhelpful narratives may that turn out to be false.

“By focusing on getting it right rather than always being right, we’re able to preserve the flexibility to change course when the fundamentals change.”

Read Amy’s full article here

Latest updates from our fund managers

Income and Fixed Interest

Tim Hext: Australia to expect state budget downgrades

June 25, 2025

See all

Emerging Markets

Emerging markets: Look past commodity exports to countries with strong domestic demand

July 26, 2023

See allSubscribe to The Point

Get regular insights on investing, market analysis and portfolio management from the experts at Perpetual Group.

Follow

The Point

These podcasts are for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. They have been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on the information, consider its appropriateness having regard to their or their clients’ individual objectives, financial situation and needs. The information is not to be regarded as a securities recommendation.

The information in these podcasts may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this presentation is complete and correct, to the maximum extent permitted by law neither Pendal nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Any projections contained in these podcasts are predictive and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

For more information, please call Customer Relations on 1300 346 821 8.00am to 6:00pm (Sydney time) or visit our website www.pendalgroup.com

Global equities: How should investors approach market uncertainty?

We’re in an “average recessionary market”, says Pendal’s Chris Lees in our latest fast podcast.

“If you don’t think there’s a banking crisis coming, then it’s actually time to gently start buying again, and that’s what we’re doing,” says Chris, who co-manages Pendal Global Select Fund.

“We’re not going into, we think, a global banking crisis market. So there are opportunities.”

“In the post-Covid, post-recessionary world, as we look forward, healthcare looks really very, very attractive.

“We’ve got some fantastic growth stocks in the biotechnology tools, the biotechnology equipment, the biotechnology outsourcing world.

“Those are fabulous businesses whose earnings have got nothing to do with oil, interest rates or the current problems in the world.”

FAST PODCAST: Where we are in this interest rate cycle

Quick view

FAST PODCAST: Where we are in this interest rate cycle

50-point rate rises are probably over for now in Australia, but investors should watch for lag, says Pendal’s Tim Hext in our latest fast podcast.

“Firstly, it takes several months for a rise to feed through to your mortgage. So given they only started in May, the full impact of rate rises won’t be felt until the end of the year around Christmas.

“The RBA will probably do two more 25s this year. They might put in a third to 3.1%, but let’s call it 3%.

“I think then they’ll sit back and see what impact it’s had. Of course in 2023 you’re going to see a lot of fixed-rate mortgages rolling into floating rates, so there’s a hell of a lot of tightening yet to happen.

“Secondly, on the goods inflation side there’s a huge amount of evidence that we’ve seen the peak in the US.

“There’s every chance we’ll get some negative CPI US prints. This doesn’t mean inflation’s over. It doesn’t mean they’re going to cut rates. But that certainly takes the pressure off.”

Sustainable fashion: would you wear socks made from wood pulp?

Quick view

Sustainable fashion: would you wear socks made from wood pulp?

If you’re like most people, your clothes are made of cotton produced with pesticides, fertilisers and hundreds of litres of water.

Or they might be synthetic, made from petroleum and destined to become ocean-borne micro-plastic.

“The fashion industry has a lot to answer for,” says Maxime Le Floch, an analyst with Regnan’s impact investing team.

“Fashion is responsible for 5 per cent of annual carbon emissions. Some 6 per cent of global pesticide production is applied on cotton crops alone.”

Austria’s Lenzing Group may have an answer. It’s making fabrics from sustainably sourced wood pulp for shirts, shorts, towels, nappies and wet wipes.

Its flagship fabrics such as lyocell (pictured) are made from cellulose, the compound that makes up the cell walls of plants. The process uses 10 times less water and produces fewer carbon emissions than polyester.

AMY XIE PATRICK: China’s going lower on rates. Here’s what it means for investors

Play podcastAMY XIE PATRICK: China’s going lower on rates. Here’s what it means for investors

As the West hikes rates, China keeps cutting, hoping to counter the impact of its Covid-zero policy and spark demand in a debt-laden property sector (see graph below).

Will Beijing continue the course? And what does that mean for investors?

China’s monetary authorities are not independent as we know them in Australia and the US, explains Pendal’s Amy Xie Patrick in our latest fast podcast.

“The central bank in China has been lowering interest rates because the economy quite frankly is in a rut.

“Most major investment bank analysts expect growth in China will fall to levels not seen over the last decade. Frankly China will struggle to get above the 4% threshold for the next year or perhaps even more.”

If these headwinds continue to build for China, and stimulus efforts continue to be piecemeal, the outlook for global fixed income could be very bullish, says Amy.

Can impact investors really help change the world? Here’s evidence from Regnan

Quick view

Can impact investors really help change the world? Here’s evidence from Regnan

Can investors really help solve the world’s biggest problems?

Regnan’s equity impact investing team says “yes” — and they lay out the evidence in their first annual impact report.

Regnan Global Equity Impact Solutions fund aims to generate market-beating, long-term returns by identifying companies that are innovating and disrupting their way to solutions for the planet’s biggest problems.

The team’s inaugural impact report shows investors in the fund are helping:

-

Train young doctors in Brazil, one of the most medically under-served countries in the world (Afya)

-

Produce low-carbon cement to transform the building industry (Hoffmann Green Cement)

-

Fight homelessness (Home REIT)

-

Develop better batteries for electric vehicles that charge six times faster (Ilika)

-

Make fabric from tree fibres to replace cotton, using less water and emitting no net carbon (Lenzing)

Impact investing: Computer simulations are helping solve big problems

Quick view

Impact investing: Computer simulations are helping solve big problems

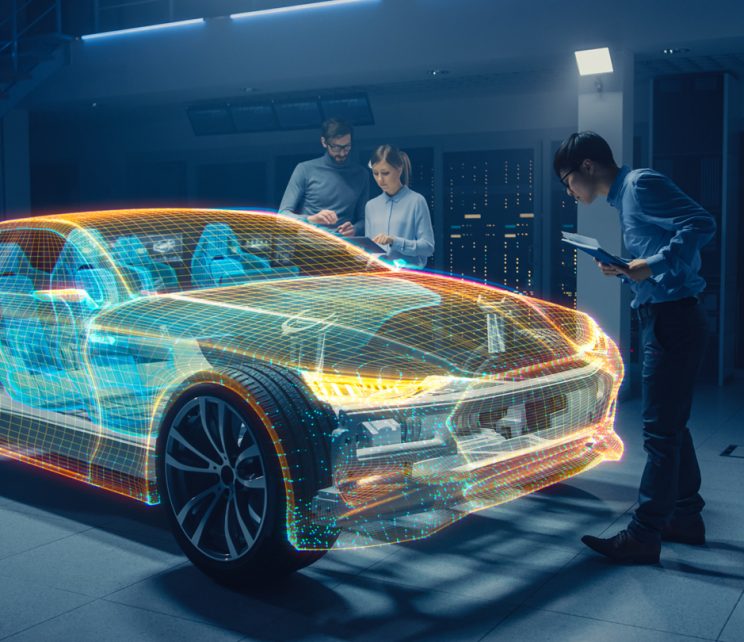

You’ve driven a car designed on a computer — but have you driven one designed by a computer?

The rising sophistication of simulation software means your next car — or at least parts of it — will have its performance simulated and tested by computer software, says Regnan’s Maxime Le Floch.

The technology is dramatically cutting the time to create and test new designs, improving manufacturing efficiency and cutting costs and resources.

“We need to speed up innovation across the global economy. This is called out by UN Sustainable Development Goals 9 and 12 which highlight resource efficiency and enhancing scientific research,” says Maxime, an analyst with Regnan’s Equity Impact Solutions team.

The software is also used in the renewable energy industry to design wind turbines.

Regnan’s Global Equity Impact Solutions fund has a position in US-listed simulation software leader Ansys, which aims to “help innovative companies deliver radically better products”.

FAST PODCAST: How to choose the right mid-cap Aussie stocks

Play podcastFAST PODCAST: How to choose the right mid-cap Aussie stocks

The development of a decarbonised economy will take a long time.

But that doesn’t mean it’s not a critical factor right now, says Pendal portfolio manager Brenton Saunders.

The ESG transition can be divided into three periods, says Brenton:

- The existing status quo

- A transition period with an overlap between old and new technologies

- A transition to the new

“Once you understand that, it’s really about characterising companies in terms of where they sit in these transitions,” says Brenton, who manages Pendal MidCap Fund.

“Are they making their way across those phases to an environment where they can contend with the decarbonised, ESG world? Or are their business models fairly constrained to one of those thematics?

“We are very careful about how and if we invest in those latter sectors because this transition will take place over the course of the next 10 years. That’s definitely within the context of an investible timeframe.”

Impact investing: How inflation is creating sustainability opportunities

Quick view

Impact investing: How inflation is creating sustainability opportunities

Higher commodity prices are triggering investor interest in companies that can recycle, process waste and optimise production to reduce costs.

That’s creating new opportunities for sustainable investors, says Tim Crockford, who leads Regnan’s Global Equity Impact Solutions fund.

Sustainable production and consumption is UN Sustainable Development Goal 12 which aims to reverse the 70 per cent growth in raw materials used in production between 2000 and 2017.

Higher inflation underpinned by soaring prices for energy, metals and food have put this UN goal at the centre of the global macroeconomic debate.

“There is obviously an environmental imperative there, but increasingly with the cost of inputs rising dramatically there is now a financial imperative,” says Tim. “It’s been a big area of focus for us in the last 18 months.”

Loading posts...

Subscribe to The Point

Get regular insights on investing, market analysis and portfolio management from the experts at Perpetual Group.