Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

Tim Hext: Australia to expect state budget downgrades

This article is more than 12 months old. Find our latest insights here

Here’s what the latest CPI data and state budgets say about the Australian economy, according to head of government bonds TIM HEXT

THE May year-on-year CPI series was released today.

The data showed headline prices 2.1% higher than May last year, with trimmed mean prices 2.4% higher.

Only two items have double-digit changes: Tobacco is up 11.5% and Fuel is down 10%. Electricity subsidies are still playing a role (electricity down 5.9% from May 2024), but this will turn sharply positive in July.

The Reserve Bank will not look too deeply into this data as it is consistent with its current forecast of 2.6% trimmed mean inflation.

Pleasingly, services inflation is now 3.3% year on year, the lowest since May 2022. The quarterly inflation numbers released at the end of July, which are the main focus of the RBA, should show goods prices around 1% and services around 3.5%.

Health and education will make further significant falls in services inflation difficult.

Inflation is not a reason to cut or not cut – but, when put together with ongoing sluggishness in consumption, allows the central bank to cut rates in July.

The market remains priced at 80% chance of a cut.

State budget downgrades are coming

New South Wales (NSW) and Queensland both issued budgets this week. Both highlighted a recent trend towards optimistic rather than conservative forecasting.

Budgets have always been part finance and part marketing, but not surprisingly – given the current zeitgeist and short attention spans – spin is everything.

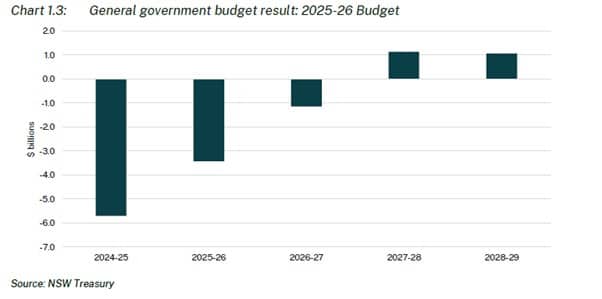

New South Wales

For New South Wales, the general government forecast budget position is improving.

The state announced a surplus – or, more accurately, hopes of a surplus – by 2027/28. This is the operating position, which is basically cash receipts, less cash payments, less depreciation.

It does not include infrastructure that can be financed either on or off budget (through debt).

The optimism comes from the forecast growth in expenses: 2.4% a year on average for the next five years.

Now employee expenses, 40% of total, are forecast to grow at 3.7%, which is consistent with recent wage rises granted of 3.5-4% a year to many public sector employees, but not consistent with growth in the number of workers.

Even if this number turns out to be accurate, it puts a lot of pressure on the other 60% of expenses to grow by around 1%. The heavy lifting is to be done by what is called ‘Grants, Subsidies and Transfer expenses’ which make up 20% of expenses and are forecast to go backwards.

We will look under the hood on this one as it is very unusual to see these go backwards absent any policy announcements.

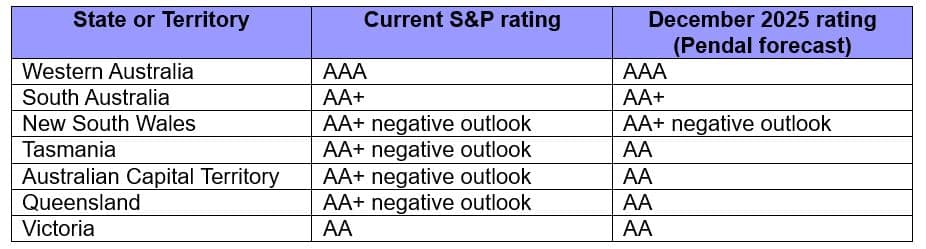

Overall, this is a treading-water budget and will leave Standard and Poors (S&P) somewhat in limbo on its negative outlook for the AA+ rating. If the government was to deliver on 2.4% expense growth, then the AA+ would stay, but there is likely to be some cynicism around this number.

Negative outlooks are not supposed to be permanent and are usually resolved one way or the other within two years. The negative outlook was put on in November last year so I suspect it stays for at least the next year.

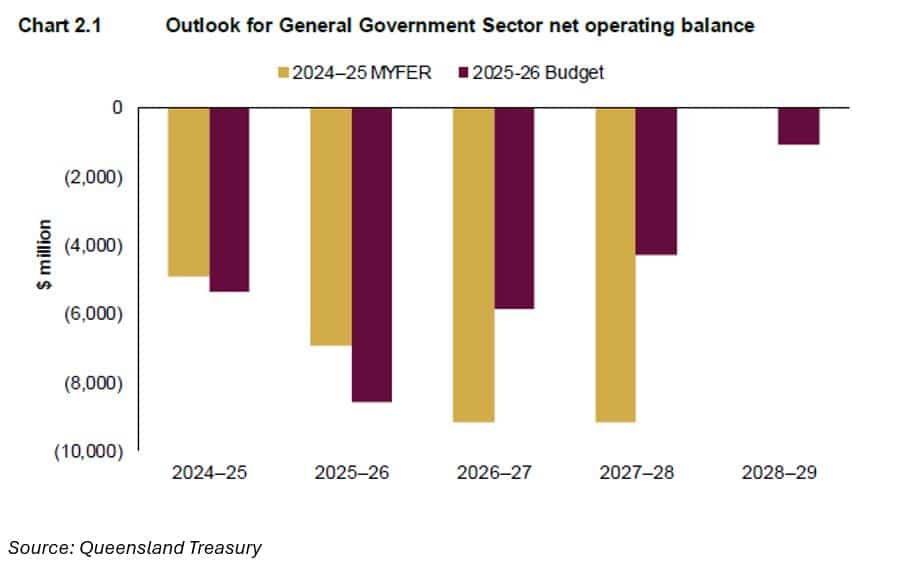

Queensland

The shambles of the Queensland mid-year fiscal update (MYFER) in January have now been uncovered as another cynical exercise in making everything look as bad as possible and then blaming on the outgoing government.

CEOs do it all the time, but you would hope for better from an elected government – particularly a government department calculating the numbers.

So how do we look at this budget?

The new LNP government are heralding it as a $6.6 billion improvement over three years from the MYEFR, driven by its responsible management. This is the chart in their budget papers.

But it is, in fact, a deterioration of around $21bn from the last budget.

No charts for that one. No doubt the previous Labour government was, as usual, too optimistic (see above in NSW) but the shock/horror revisions in January went from Pollyanna to Cassandra in one move.

Now, after the MYEFR, the new government probably hoped Queensland would be downgraded by S&P – the thought is to get it out of the way and easily blame it on the last crew. In fact, the forecast debt revisions in January were even more spectacular than the budget revisions, clearly blowing Queensland way below the AA+ thresholds.

However, S&P didn’t play ball – merely putting Queensland on negative outlook in February and putting the onus on the new government to fix it.

Well, in our humble view, the government has not done enough to “fix it”.

By our calculations, it will still see Queensland trickle down to AA – even if not blowing down. Put another way, the new government is more fiscally responsible than the old one, but not enough to keep the AA+ rating.

Anyway, for those still reading, we think the Australian state ratings with S&P will look something like this by year’s end. Note: S&P does not rate the Northern Territory.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

The team won Lonsec’s Active Fixed Income Fund of the Year award in 2021 and Zenith’s Australian Fixed Interest award in 2020.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current at 25 June 2025. PFSL is the responsible entity and issuer of units in the Pendal Monthly Income Plus Fund (ARSN: 137 707 996) and Pendal Dynamic Income Fund (ARSN: 622 750 734) (Funds). A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com