Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

Tim Hext: What Trump’s tariff formula means for markets

This article is more than 12 months old. Find our latest insights here

The US has announced a slew of tariffs based on a reciprocal tariff ‘formula’. Head of government bond strategies TIM HEXT breaks down the latest

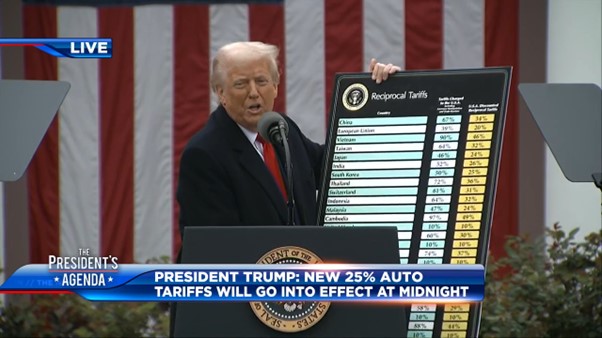

TODAY, President Trump announced a baseline 10% tariff on all goods into the US. This was widely expected.

Less expected, however, was the basis for “reciprocal” tariffs.

You would be forgiven for thinking this meant that whatever rate of tariff other countries imposed on the US, the US would impose back.

After all, Trump’s tariff board said “Tariffs charged to the US”.

However, rather than being actual tariffs, they made up a number based on a reciprocal tariff formula – that is, the trade deficit that the US has with a country divided by the size of imports the US takes from that country.

For example, Indonesia has a trade surplus (deficit for the US) of $17.9bn on total exports (imports for US) of $28 billion – so, its supposed tariff on the US is 64%.

What this highlights is that the US is more focused on their poor current account position and will use tariffs to fix it.

This meant the reciprocal tariffs being imposed by the US were higher than most expected, with markets reacting with an old-fashioned risk-off move.

What do these tariffs mean for the US economy?

There is more to play out as bilateral trade talks take place, so final tariffs may yet soften. Mexico and Canada were not mentioned today, but both still await 25% tariffs.

However, the current net increase in tariffs for the US is around 20%, translating to around an extra 2% to inflation. Part of that may be absorbed by exporters or retailers, but it would be hard to see inflation not being hit by at least 1%.

For growth, the US consumer is 70% of their economy.

If consumers spend the same amount of money, their volume of consumption would fall – leading to a roughly 1% lower GDP than anticipated. Employment should be softer near term as the boost from onshoring will take longer to come through.

Put together, we have stagflation-lite in 2025.

The US Federal Reserve is caught between higher inflation and lower growth, but would more likely see through the one-off inflation impact and react to the lower growth.

The Fed Funds Rate may yet end up near 3%, or “neutral”.

What about Australia?

We have a small trade deficit with the US. Under the Trump formula, our $14bn deficit on $88bn of imports should mean we tariff the US 16%.

Try that for “reciprocal”. Alas, Prime Minister Albanese is not one for such moves.

Our economy will take any hit through Asia, especially China. Almost 90% of our exports go to Asia, so any slowdown there will have an impact here.

However, we should not see any direct inflation hits. In fact, exporters may look to replace some US demand in other markets, which could even see some import prices fall.

Australian financial markets, however, will continue to be buffeted by global events.

Finally, bonds may once again perform their role as a defensive instrument. Today’s moves offer some hope.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

The team won Lonsec’s Active Fixed Income Fund of the Year award in 2021 and Zenith’s Australian Fixed Interest award in 2020.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current at 3 April 2025. PFSL is the responsible entity and issuer of units in the Pendal Monthly Income Plus Fund (ARSN: 137 707 996) and Pendal Dynamic Income Fund (ARSN: 622 750 734) (Funds). A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com