Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

Samir Mehta: How luxury stock Prada is making a fashionable comeback

This article is more than 12 months old. Find our latest insights here

Despite a recent lull in the luxury segment, one iconic brand is making a comeback. Pendal’s SAMIR MEHTA outlines a fashionable investment opportunity

- A well-established brand that encountered tough times

- Prada’s youth brand Miu Miu leads a turnaround

- Find out more about Pendal Asian Share Fund

IN THE film The Devil Wears Prada, Miranda Priestly – the formidable editor-in-chief of Runway Magazine – sarcastically declares: “Florals, for spring? Groundbreaking.”

Miranda personifies an uppity, sceptical and dismissive know-it-all, putting down any style trend that she was not the first to spot.

Identifying turnaround stocks requires a similar type of scepticism.

These days I’ve mostly eschewed the practice, but one type of turnaround story still catches my interest – a well-established brand encountering tough times.

And Hong-Kong-listed, Italian luxury brand Prada is one such case.

Back in fashion

The century-old fashion house was recently flagged as an opportunity by one one of our in-house investment screens which looks for improvements in incremental operating and free cash flows.

Between 2016 and 2019, Prada’s financial performance was anaemic.

A reliance on wholesale distribution (as opposed to retail), undesirable store locations and rudimentary online marketing efforts didn’t help.

But all was not lost.

Find out about

Pendal Asian Share Fund

Prada is an established brand with a founder-led team (owning 80% of the business) and a long-term commitment to fashion, legacy and – importantly – a willingness to hire professionals.

Prada generated minimal operating cashflows but had low debt (other than committed leases).

Stagnant sales and low profit margins stood starkly against the might of France’s LVMH — the world’s biggest luxury goods company.

A lull in luxury

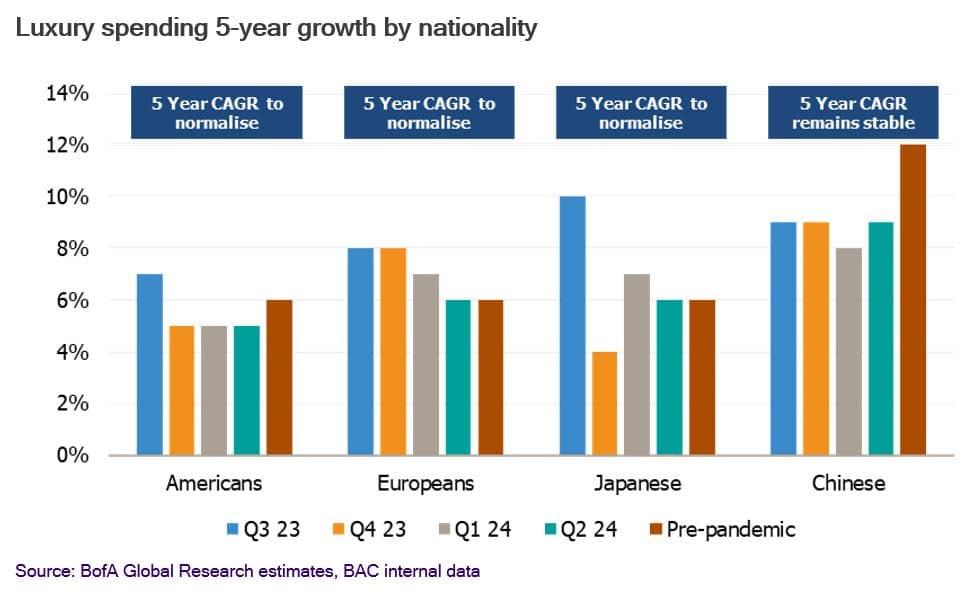

In recent years the pandemic, government stimulus, and inflation have somewhat reshaped the luxury industry.

Pre-pandemic, Chinese consumers were the driving force for luxury goods.

During and post-pandemic, demand was fuelled largely by Western consumers assisted by government stimulus and a shift in spends from services to goods.

In 2023 and 2024, inflation and rising interest rates dented disposable incomes.

Perhaps most underestimated was the moderation of demand in China.

A slower economy, poor job market, falling property values, and a clampdown on conspicuous consumption by the Chinese Communist Party became strong headwinds.

In a way, Prada is lucky for its marginal presence in the US, where luxury spends have come off the sharpest in 2024.

Industry-wide, sales growth polarisation between brands seems to have further accelerated.

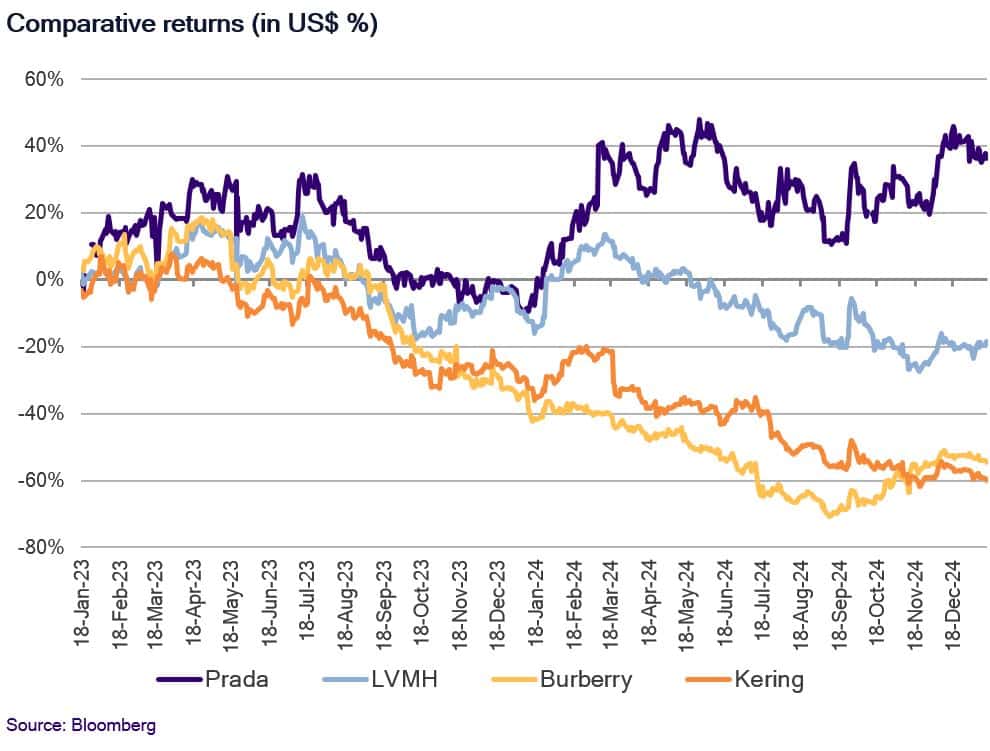

Prada, Hermes and Brunello Cucinelli still delivered double-digit revenue growth in 2Q24, while some brands in turnaround remained under significant pressure (Gucci and Saint Laurent within Kering, as well as Burberry and Swatch Group), with sales down in double-digit territory.

Margin pressures were exacerbated by currency headwinds, particularly from JPY and RMB, and 1H24 EBIT for the sector declined 11% year over year.

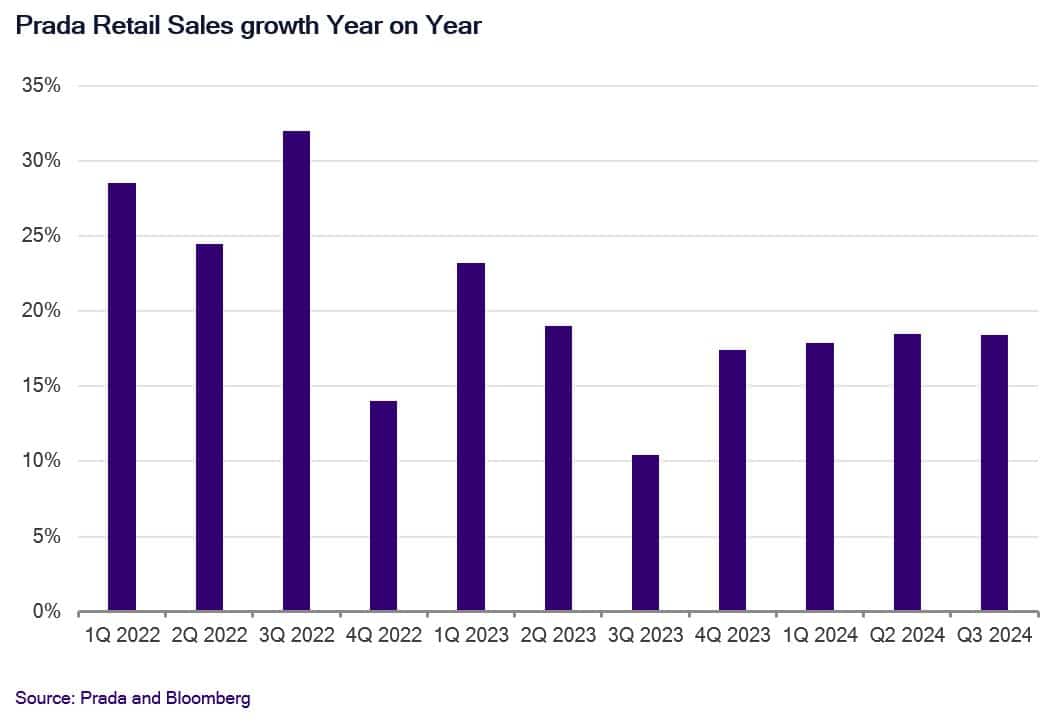

Prada bucks the trend

In Prada’s case, a confluence of factors over the past five years seems to have made a marked difference.

A shifting away from wholesale distribution meant an initial disruption in sales. But once accomplished, this tactic brought better control over inventory and pricing.

The business revamped its online marketing and influencer engagement.

Millennials and Gen Z – once dismissed as fickle – became the new darlings of luxury retail.

Prada courted them not with “florals for spring”, but with sustainability initiatives and inclusive marketing.

It spoke the language of the young – not in patronising tones, but with the authenticity of a brand reinventing itself.

Product mix was another key factor.

Prada and its youth brand Miu Miu (founded in 1992), diversified their offerings, creating a balanced portfolio.

They refocused on craftsmanship and heritage. And in today’s world of fast fashion and disposable trends, Prada doubled down on quality – embracing its history not as a burden, but as a differentiator.

A changing season

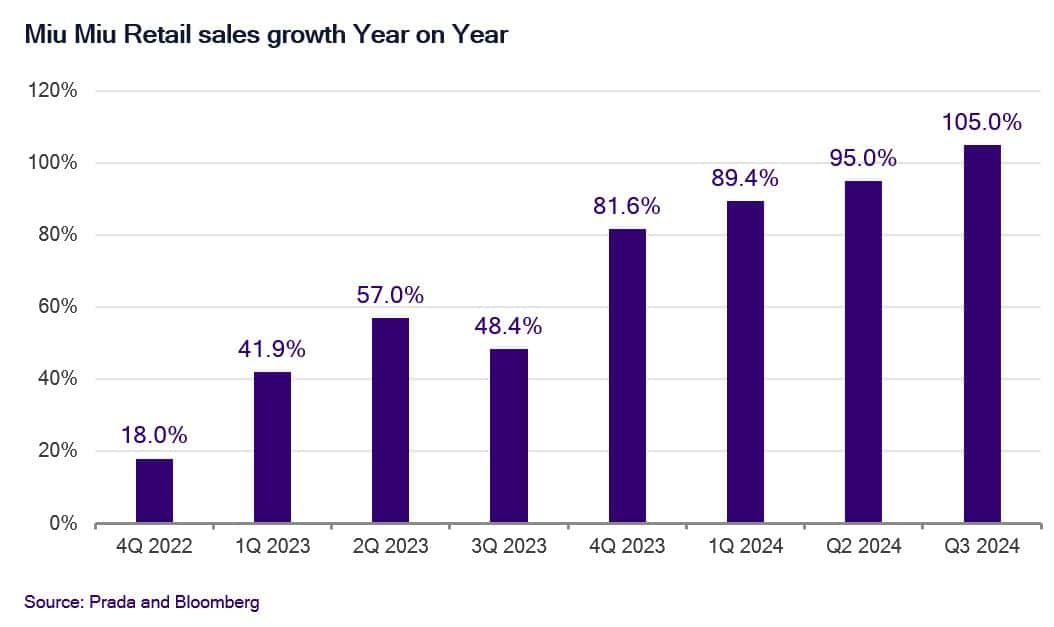

Miu Miu – historically a small brand within the Prada Group which rarely surpasses €500m in annual revenues – has struck a chord among the younger generation of shoppers.

Yes, we do expect brands – sometimes out of nowhere – to gain traction in a social media influencer-dominated world.

But for a 33-year-old brand to achieve this sort of growth is staggering (see below).

Needless to say, with a high base, Miu Miu’s revenue growth in 2025 will see a moderation.

Besides, we need to monitor how sustainable this supercharged growth is, particularly when the luxury industry at large is struggling.

If it has the brand pull, which leads to growth of 20-25% in 2025, the margin expansion should be a positive upside too.

Out of the way, Miranda Priestly

Ultimately, similar to any business, the right people make all the difference.

Prada founders Patrizio Bertelli and Miuccia Prada (aged 78 and 75, respectively) made several changes to the management team.

Their elder son Lorenzo joined in 2017 and is now group CMO. A highly experienced management team (including Andrew Guerra as group CEO, Andrea Bonini as CFO and Gianfranco d’Atttis Prada as brand CEO) were appointed in 2022 to further bolster the team.

On the creative side, the 2020 appointment of Belgian designer Raf Simons as co-creative director of the Prada brand (alongside Miuccia Prada) seems to have boosted creativity and commerciality, while also ensuring a stable succession plan for Ms Prada over the longer term.

Simons previously worked with Jil Sander, Christian Dior and Calvin Klein while running his own label.

From all accounts, Ms. Prada and Raf Simons’ joint collection (starting in 2021) were well received by fashion critics.

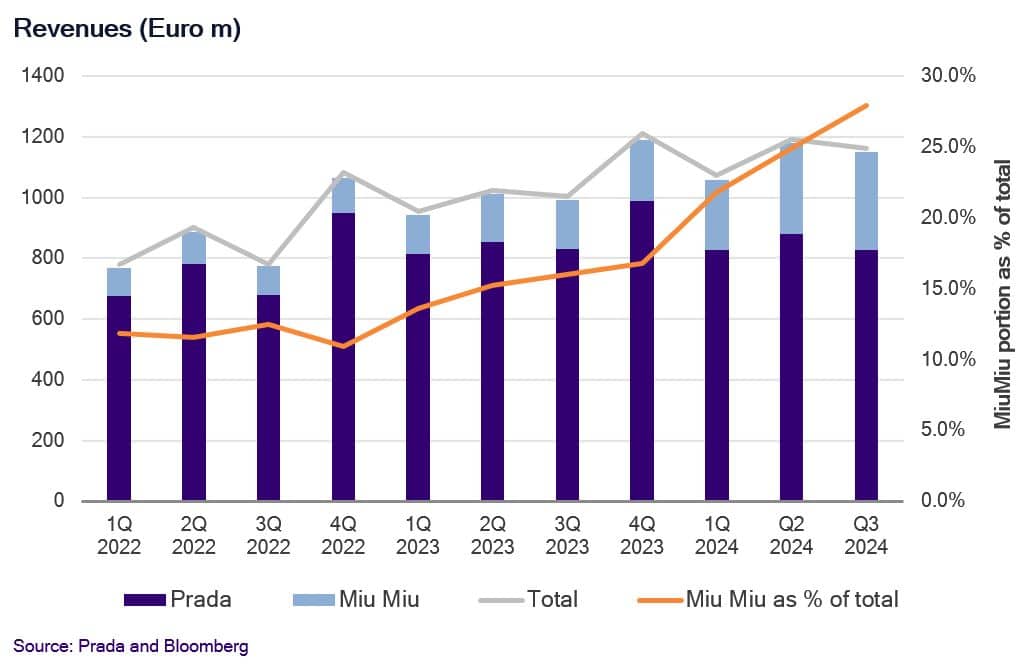

In 2024, all geographies grew in the double digits – Europe at 18%, APAC at 16% (China was low double digits), Japan at 46% (with mainly Chinese tourists) and the Middle East at 15% – with the exception of the except US, which grew 9%.

Miu Miu remains the star with 90% growth.

The younger brand is now almost 22% of total revenue and at its current run rate could see €1b in annual sales.

Fashion forward forecasting

To demonstrate such strength globally during a challenging period for the industry is an achievement.

There is no room for complacency in any business, let alone fashion.

It is fitting that there are rumours of a sequel to The Devil Wears Prada.

If it went ahead, I wonder whether Priestly might climb down from her high horse and acknowledge the new kid on the block.

The Devil Wears Miu Miu?

Either way, we wait to see if the markets recognise Prada for its resilience and renaissance and afford it much higher multiples than it has in the past.

About Samir Mehta and Pendal Asian Share Fund

Samir manages Pendal’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Perpetual Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current at January 20, 2025. PFSL is the responsible entity and issuer of units in the Pendal Asian Share Fund (Fund) ARSN: 087 593 468. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com.

The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance.

Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.

For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com