Close

Leave Feedback

Welcome to the new btim.com.auTake a two minute tour to see what we've changed

Hi there! Welcome to the new look Pendal website... Take a two minute tour to see what we’ve changed.

Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

Anna Hong: What’s next for rates after RBA loses patience

What’s next for rates now the Reserve Bank has lost its patience? Assistant portfolio manager ANNA HONG explains

THE Reserve Bank this week took a small step towards a June rate hike.

In February and March, Governor Phil Lowe’s monthly statements referred to the board’s willingness to be “patient” as it “monitors how the various factors affecting inflation in Australia evolve”.

This month the word “patient” was conspicuously absent — though the omission was anticipated by the market.

“Over coming months, important additional evidence will be available to the board on both inflation and the evolution of labour costs,” Dr Lowe said.

“The board will assess this and other incoming information as its sets policy to support full employment in Australia and inflation outcomes consistent with the target.”

Some are expecting a hike in May. But the reference in this month’s statement to upcoming inflation data on April 27 and wages data on May 18 suggests a pre-election rate rise in May is unlikely.

It’s more likely next month’s statement will feature a further change of language that paves the way for a rate hike in June.

Only twice in Australian history has the RBA changed interest rates during an election — the first was a rate hike, the second a rate cut.

Find out about

Pendal’s Income and Fixed Interest funds

Both times there was a change in government.

Dr Lowe declined to cut rates in May 2019 — just 11 days before the last federal election — even though unemployment was drifting higher.

We expect this time will be no different.

The first election rate change occurred in November 2007.

Back then RBA Governor Glenn Stevens decided to raise interest rates 17 days out from the election to manage rising inflation.

This action — and two more rate hikes in early 2008 — helped Australian inflation peak in September 2008. Though the global financial crisis may have played a bigger role.

There are similarities between our current state and November 2007.

But inflation is now more supply-side led. And the RBA has this time chosen to remain dovish for longer, continuing to leave cash rates at 0.1%.

Despite that, the banks are already repricing for the future.

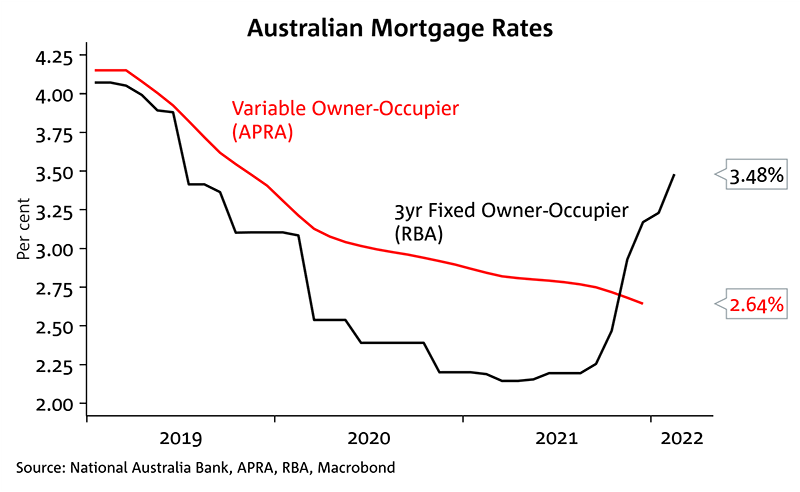

Advertised fixed rates have risen more than 60% from an average of 2.14% to 3.48%, according to APRA and RBA data.

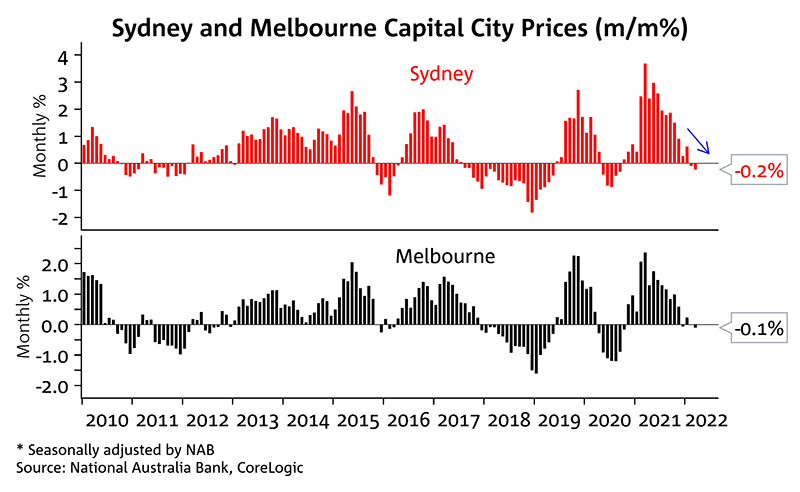

In addition, the serviceability buffer was raised from 2.5% to 3% in the new home loan assessments.

This has led to Sydney and Melbourne house prices cooling off, signalling that a phase of high capital gains may be behind us.

With a surge in fixed-rate borrowing well and truly behind us, variable rate rises are not far away.

The market is predicting more than 3% of rate hikes in the next few years. If that’s correct it will be interesting to see how mortgage holders cope.

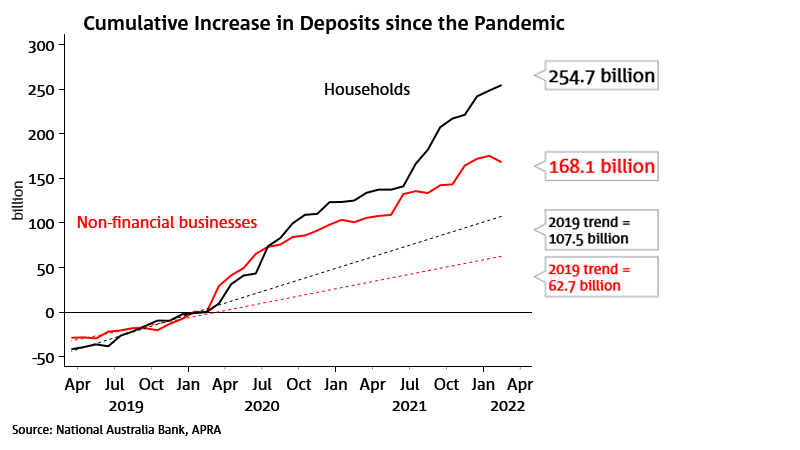

Household deposits continue to rise — up $255 billion since the pandemic — indicating Australian households have a war chest to cushion the blow.

But that’s not necessarily good news.

Delayed action in tackling inflation may result in a long, drawn-out battle to curb price rises fuelled by supply chain issues.

Will the supply chain issues ease sufficiently to prevent a protracted rate hike cycle?

The RBA will be cautiously watching this dynamic.

Looking ahead, we have the RBA Financial Stability Review coming up, in addition to the NAB Business Conditions and CBA Household Spending Intentions.

We are keen to understand the RBA’s assessment of the impending mortgage stress and its concerns around the ability of the wider economy to withstand rate rises.

NAB Business Conditions and CBA Household Spending Intentions will provide a good gauge on forward-looking business and consumer confidence.

If those indicators remain elevated we may see costs of living get another leg up.

Portfolio implications

For many investors, the current dilemma in portfolio decisions relates to the relative importance of the geopolitical instability in Europe versus the inflation trajectory.

With Australian Government 10-year bonds appearing to have found support in the 2.8% to 3% range, a balanced portfolio can increase its defensiveness knowing that most of the inflation concerns are already priced in.

Furthermore, 10-year real yields are now positive (more than 0.3%).

That carry can provide good protection for investors.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at April 7, 2022.

PFSL is the responsible entity and issuer of units in the Pendal Monthly Income Plus Fund (ARSN: 137 707 996) and Pendal Dynamic Income Fund (ARSN: 622 750 734) (Funds). A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund.

An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.

For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com

Keep updated

Sign up to receive the latest news and views